- Fintech

KYC & KYB in fintech: best practices

The financial services industry is experiencing a disruptive digital transformation. Many services have moved online, calling for a robust system for customer identity verification.

KYC and KYB appeared in response to growing concerns over money laundering, fraud, terrorism financing, and other forms of financial crime. They became formalized due to regulatory pressure and the practical need to protect the integrity of the financial system.

What is the role of KYC and KYB in fintech? What are the challenges of implementing these procedures? What can financial companies do to make the customer onboarding experience smooth and efficient? Read on to discover answers to these and other questions.

Understanding KYC & KYB: definitions and significance

KYC and KYB are integral components of a financial institution’s or fintech company’s AML (Anti-Money Laundering) and counter-terrorism financing (CTF) obligations and are required by regulatory authorities in many jurisdictions. Let’s take a closer look at these concepts.

What is KYC?

A critical component of the customer due diligence process, KYC, or Know Your Customer, refers to the procedure banks, fintechs, and other financial institutions use to confirm the identity of their individual customers. The aim of KYC is to prevent money laundering, terrorist financing, financial fraud, and other financial crimes.

At its core, KYC helps verify that the people using a service are who they say they are. It typically involves collecting personal details like full name, address, and date of birth and asking customers to upload a government-issued ID, often paired with a selfie for facial match verification.

Depending on its risk profile and target market, a fintech provider might also need to integrate tools for address validation, biometric verification, or politically exposed persons (PEP) screening.

KYC isn’t optional if you want to launch a fintech product in regulated markets. In the US, it’s part of the Customer Identification Program (CIP) under the Patriot Act. In the EU, it falls under the Anti-Money Laundering Directive (AMLD), and in the UK, it’s enforced through the Money Laundering Regulations overseen by the Financial Conduct Authority (FCA). In practice, this means you need to think about KYC from the design stage.

What is KYB?

Fintechs serving business clients need to implement KYB, or Know Your Business, checks. While KYC and KYB are similar in purpose, the KYB processes are tailored to verifying the identity of businesses rather than individuals.

KYB involves verifying that a company is legally registered and identifying the people who actually own or control it. This typically means collecting business registration details, tax IDs, company addresses, and director information. Fintech companies also need to identify and screen ultimate beneficial owners (UBOs) – the individuals with significant ownership or control, even if they’re not listed as company officers.

KYB helps prevent a platform from being used by fake companies, shell corporations, or business entities tied to money laundering. From a product and reputational perspective, it builds trust – regulators, payment partners, and end-users expect the business onboarding process to be thorough and secure.

Regulatory requirements for KYB vary from country to country, but the core principles remain the same: financial institutions must verify the legitimacy of all business entities they work with and identify the individuals who ultimately control them.

In the US, KYB falls under the Bank Secrecy Act and is reinforced by FinCEN’s Customer Due Diligence (CDD) Rule, which requires identifying ultimate beneficial owners (UBOs). In the UK, KYB requirements are set out in the Money Laundering Regulations 2017 and enforced by the Financial Conduct Authority (FCA). In the EU, KYB is governed by the Anti-Money Laundering Directives (AMLD), with enforcement carried out by each member state’s designated financial authority.

Key challenges in KYC & KYB processes

Implementing KYC and KYB procedures comes with some challenges. While the KYC and KYB processes are essential for regulatory compliance and risk management, they can also create friction for users and require significant backend infrastructure. Below are some of the common pain points companies face when dealing with individual and business verification.

For KYC

1. Complex customer data and documentation requirements

Users may upload incomplete or outdated identity documents, use names that don’t match official records, or run into problems with address verification. Things get even trickier when you need to support multiple languages and document formats.

2. Ensuring a seamless and secure verification process

Users expect the onboarding process to be fast and frictionless, while regulators require thorough identity verification. If the KYC procedure is clunky or invasive, people may abandon the process. On the other hand, cutting corners can leave your platform exposed to the risk of fraud or compliance failures.

3. Balancing regulatory compliance with customer experience

KYC is mandatory, but how you implement it matters. A rigid or overly manual process can frustrate users, adversely affecting conversion rates. The challenge is designing a KYC process that satisfies legal requirements without compromising on customer experience.

For KYB

1. Verifying ownership structure and the legitimacy of businesses

Unlike individuals, businesses don’t have a single form of ID. You may collect data from registries, licenses, and legal documents and still be left without a clear picture of who’s really in control. Identifying UBOs (Ultimate Beneficial Owners) adds another layer of complexity, especially with shell companies or layered ownership.

2. The challenge of dealing with cross-border business verification

When your platform serves businesses across different geographic locations, verifying them can become a logistical headache. Public registries vary in accessibility, format, and trustworthiness. Legal terms differ, naming conventions change, and the documentation may not be available in a language your system can handle.

3. Implementing ongoing monitoring to catch suspicious changes

KYB isn’t a one-time task. Businesses evolve, merge, or change owners, and failing to keep up with those changes can open the door to compliance risks. Ongoing monitoring is necessary to catch red flags, such as sudden changes in business ownership structures or ties to high-risk countries, though automating this at scale can be challenging.

Best practices for streamlining KYC & KYB workflows

Efficient KYC and KYB processes are critical not only for meeting financial regulations but also for maintaining operational scalability and user trust. Here are some strategies that help financial institutions build more robust onboarding and verification flows.

Automation and digital tools

Manual checks slow things down and make the KYC and KYB processes prone to errors. Automating identity verification and data collection accelerates onboarding, reduces operational costs, and improves accuracy. Tools like API integrations with government databases, document scanning software, and AI-driven risk scoring can take much of the manual work off the team. Moreover, automating KYC and KYB also reduces turnaround time for customers, contributing to a better customer experience.

Multi-layered verification

A solid KYC or KYB process should include multiple checkpoints, such as document checks, biometric verification, and database cross-referencing. For KYB onboarding, that also means assessing UBOs, sanctions lists, and geographic risk factors. Layering your verification checks helps catch potential risks early without adding unnecessary friction for legitimate users and legal entities.

Ongoing monitoring

Verification isn’t a one-and-done task. People move, business owners change, and new regulations appear. Setting up systems for ongoing monitoring helps financial providers stay compliant and catch suspicious patterns before they grow into issues. It’s especially important for companies working with business clients, where ownership structures can shift quietly in the background unless you’re keeping an eye on them on an ongoing basis.

Customer experience

While compliance requirements are non-negotiable, a clunky verification process can discourage users before they even begin. That’s why it’s crucial to make the process feel seamless, which you can achieve through real-time feedback, mobile-optimized flows, and clear guidance at every step. When customers don’t understand why certain information is being requested, they’re more likely to drop off.

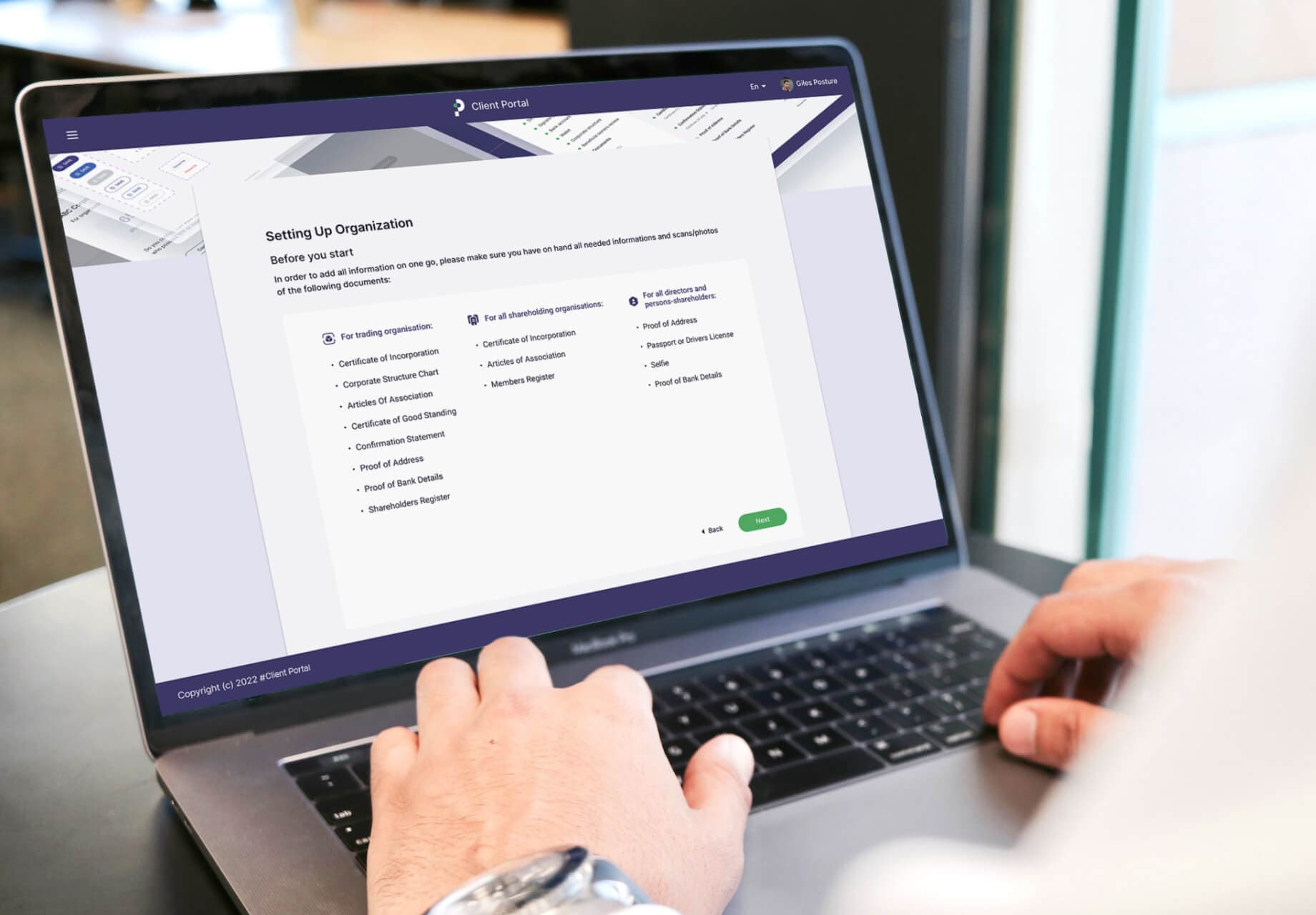

Real-world example: streamlining KYB with DeepInspire’s business identity verification solution

A UK-based digital asset execution platform turned to DeepInspire for help in finding a better way to manage its growing KYB workload. The company serves institutional clients handling large-volume crypto trades and offers a secure, private environment with transparent pricing. However, as their customer base expanded, the existing KYB flow became a bottleneck. Confusing forms, repeated back-and-forth with compliance officers, and frequent errors led to wasted time on both sides.

After interviews with stakeholders and detailed user research, the team at DeepInspire created a KYB solution that replaced scattered forms with a step-by-step flow. Each section was broken down into smaller, clearer tasks with built-in instructions and visual feedback. Users could now track their progress and understand exactly what information was needed and why.

To support the compliance team, we also built a centralized review system. This new workspace allowed officers to manage all documentation for a business in one place, view status updates, leave internal comments, and track the history of submitted changes.

The result was a cleaner, more intuitive business identity verification solution that cut down on mistakes, reduced the time of onboarding, and improved communication.

Final words

If you’re planning to build a fintech software solution, take care of the KYC/KYB process from the outset. While compliance and protection against financial crimes are the key reasons to implement identity verification, it’s important to ensure that the onboarding process is smooth and doesn’t affect user experience.

Thanks for reading!

DeepInspire / boutique software development company