- Fintech

Design thinking in financial services: a smarter way to build fintech apps

The current economic environment is undergoing a major shift. The de-banking era is reshaping how people manage their money, creating opportunities for fintech companies to win markets. Still, many fail to stand out. Too often, businesses prioritise their goals over fintech user experience, resulting in products that fall short of expectations. In many cases, it is also difficult to balance customer centricity with complex financial regulations.

This is where design thinking bridges the gap. It blends analytical thinking with creative exploration, offering a human-centred approach that puts people first.

At DeepInspire, we apply design thinking to build intuitive financial products that align business goals with customer needs without compromising regulatory compliance. In this article, we share our insights on how to unlock growth through design thinking, explore practical use cases, and examine common mistakes to avoid.

The fintech challenge

The emergence of fintech startups has raised customer expectations, and a single mistake in fintech product design can lead to lost customers or regulatory trouble.

Add to that the variety of audiences the banking sector and fintech companies serve. A product might serve a student sending their first international payment, a retiree managing savings, and a corporate treasurer moving millions, sometimes all through the same interface.

It often happens that product teams add features without rethinking the experience, which can result in onboarding processes that feel like an obstacle course, interfaces that bury essential actions under jargon, or tools that ignore the needs of people outside the most profitable segments.

In high-stakes contexts like lending or investment, this inconvenient disconnect can push people away entirely. Traditional development cycles rarely fix the problem. Requirements get defined early, based on assumptions, and months pass before users see anything. Unfortunately, it’s often too late to change anything when user feedback arrives – budgets are spent, and teams have little room to adapt.

What is design thinking in financial services?

Design thinking in fintech refers to a human-centred, iterative problem-solving approach that emphasises understanding user needs to develop innovative solutions. In simple words, it’s a way to look at problems through the customer’s eyes and work toward answers that meet both regulatory demands of the banking industry and human expectations. Instead of jumping straight to solutions, the process begins with understanding the people who will use them.

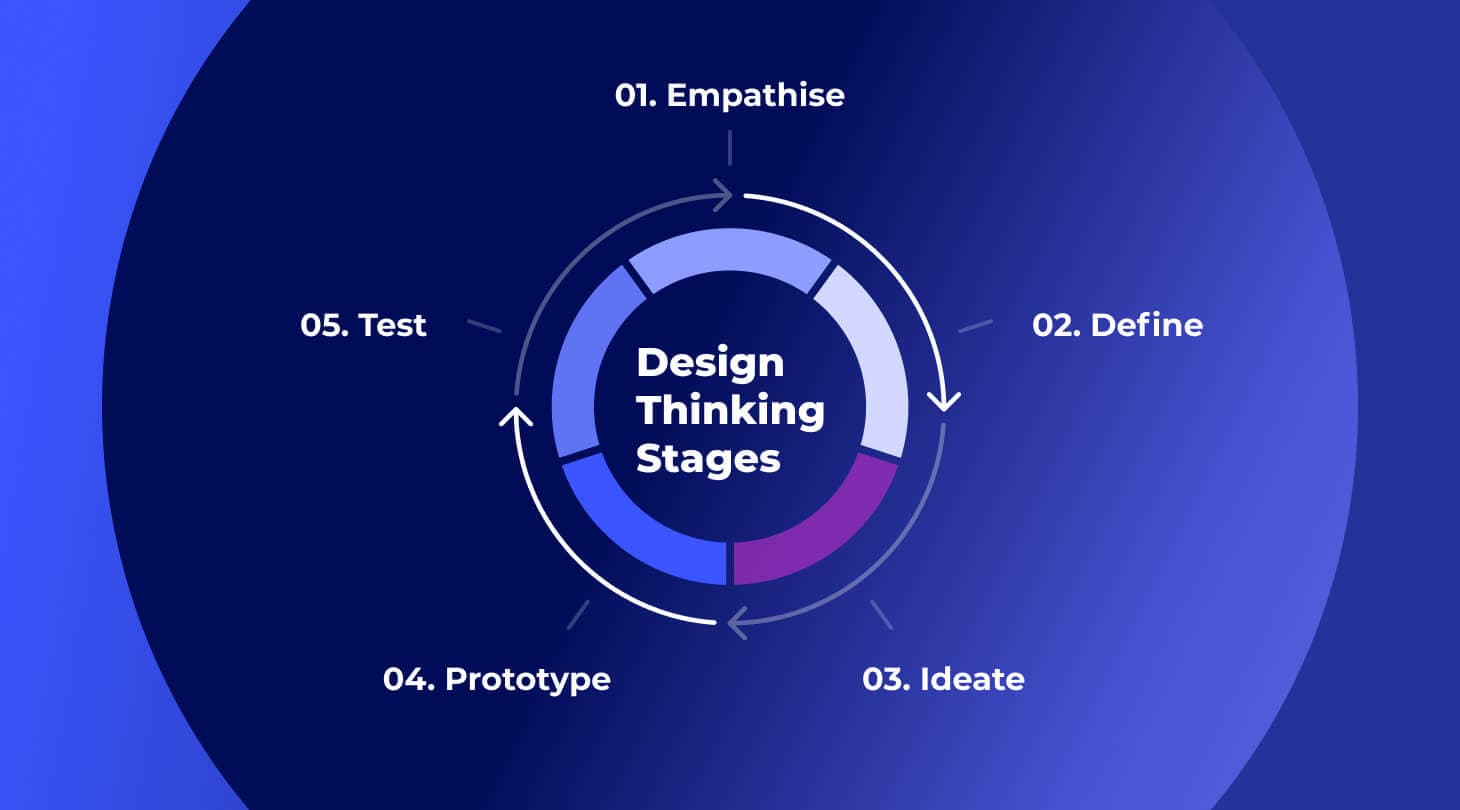

Design thinking typically follows five stages:

- Empathise. Understand the people you are building for. Beyond surveys and metrics, it involves spending time with real customers, watching how they interact with forms, dashboards, and verification steps, and, importantly, listening for frustrations.

- Define. Narrow the focus to the problem that matters most. A vague goal like “make onboarding better” becomes “cut the number of business applicants who drop off during ID verification.”

- Ideate. Generate multiple ways forward, even if some feel unconventional. A few minutes of open brainstorming can surface an approach no one expected.

- Prototype. Teams can launch MVP versions to validate concepts with real users before investing in full-scale development.

- Test. Put the prototype in front of actual users, observing where they hesitate and what they understand. Testing with users supports data-driven decisions that improve adoption rates.

The strength of design thinking in fintech lies in its cycle. Insights from testing can take you back to redefining the problem or rethinking the prototype. It values speed, empathy, and evidence over rigidly following a fixed plan.

Compared to traditional product development, which often locks in requirements and delivers in one long run, design thinking assumes that the first answer will not be the final one. It treats user feedback as a constant input rather than a post-launch correction.

Why fintech teams need design thinking

In the financial services sector, where development time is expensive and compliance updates can force sudden pivots, design thinking offers some practical advantages:

- Reduced waste. Building features that nobody uses is quite common in fintech. Early user involvement helps teams avoid investing in the wrong direction.

- Faster path to product-market fit. Iterative cycles mean you test real use cases sooner and adjust based on evidence, not speculation.

- Better adoption and retention. Products shaped around genuine needs feel easier to adopt. It goes without saying that people are more likely to stay with tools that reduce effort and uncertainty.

As you can see, design thinking in fintech delivers benefits that are anything but abstract – they directly affect revenue and a product’s ability to compete in crowded markets.

Practical applications of design thinking in fintech

Onboarding & KYC/KYB flows

Banking industry regulations demand identity checks, such as Know Your Customer (KYC) for individuals and Know Your Business (KYB) for companies. However, long or confusing verification steps drive users away. Design thinking helps simplify these flows, making compliance seamless without compromising on security.

A design-led approach starts with mapping where users stall. Do they abandon the process when asked for certain documents? Do they struggle with scanning IDs? Rapid prototypes can test simpler upload options, clearer progress indicators, or staged verification that lets people start using parts of the service before full approval.

Financial dashboards & reporting

Complex financial data overwhelms most users. Spreadsheets full of codes and figures aren’t always helpful in deciding whether to spend or wait. By focusing on how different users make decisions, design thinking can guide the transformation of raw data into clear visuals and prioritised alerts, for example, real-time performance charts with risk indicators for traders, streamlined financial reporting tools for financial advisors, or cash-flow graphs that predict shortfalls for small business owners.

Whatever the use case, the main principle of fintech dashboard design remains the same: deliver meaning, not only numbers.

Mobile banking & investment apps

Consumer apps have set high expectations – people want fast, obvious navigation and minimal errors. In the banking sector, failing to meet that standard feels riskier because money is at stake. By observing how people use an app in daily life, product teams can gain an understanding of how to remove friction points.

For example, simplifying how users switch between accounts, making confirmation messages unmissable, or allowing quick access to support without leaving a transaction screen can reduce drop-offs and support requests.

Lending & credit scoring tools

From a user’s perspective, lending decisions can seem like a mystery, and a rejection without any explanation damages trust. Through empathy work, teams can find out where transparency matters most and how to deliver it without drowning users in legal language.

This might be a plain-language summary of why a score is low, what can improve it, and how long changes might take to show. Clear communication helps people feel respected and in control, which can encourage them to reapply rather than give up.

Internal tools for Ops & compliance teams

Fintech chiefly focuses on customer-facing products, overlooking internal customers. If internal tools are slow, hard to navigate, or overly manual, employees waste hours, and morale drops.

Design thinking sessions with internal staff can uncover repetitive tasks ripe for automation, or interfaces that hide critical alerts under clutter. Well-designed internal platforms also make individual responsibilities clear, so critical compliance steps aren’t missed. As a result, refining these systems improves efficiency and reduces the chance of costly compliance errors.

Real-world example: how DeepInspire used design thinking to accelerate innovation for Experian UK&I

When new legislation opened a strategic opportunity in financial crime prevention, Experian UK&I needed to move fast. With just two months before their flagship conference, they partnered with DeepInspire to turn a high-level concept into a product that could be validated with real users.

We applied design thinking from day one – running focused discovery sessions, mapping user pain points, and co-creating several solution concepts with key stakeholders. In just four weeks, we delivered a high-fidelity, clickable prototype designed to meet both user and business needs.

The prototype was unveiled at Experian’s annual conference, attracting interest from major UK banks and generating over ten strong business opportunities. It helped validate the product direction early and created momentum for full-scale development.

Common design thinking mistakes in fintech

Even with good intentions, fintech teams can fall into traps that weaken the results of design thinking.

One of the most damaging is skipping the empathy phase. In financial services, the temptation to move fast, especially under pressure from deadlines or stakeholders, can push teams straight into building. Without a real understanding of how people experience a process, the end product often misses the mark.

Another mistake is treating compliance as something to add at the end. Regulatory requirements need to be part of the conversation from the start. Otherwise, teams risk rework, launch delays, and frustrated users.

Some teams also over-index on aesthetics at the expense of usability. A sleek fintech UI design that hides key actions or makes basic tasks harder has nothing to do with progress. In fintech, trust and clarity matter more than visual novelty, and this is function that should lead form.

The takeaway: start small, stay user-focused

Design thinking is more than a “nice to have” in fintech app design. Actually, it can become a competitive advantage in the banking industry. Teams that put users first and integrate feedback loops into their process tend to deliver products that gain trust faster and keep it longer.

The safest way to start is small. Pick one process with measurable friction, test changes early, and keep returning to the user’s perspective, even when deadlines loom.

To put it short, start small, test often, and stay user-obsessed.

FAQs about design thinking

How does design thinking differ from agile in fintech product development?

Agile is a way of organising work into short, repeatable cycles that deliver incremental improvements. Design thinking is a way of discovering what to build in the first place. Agile focuses on speed and adaptability in delivery, while design thinking focuses on uncovering the right problems and shaping solutions around real user needs. The two can work together: design thinking can feed insights and prototypes into agile sprints, ensuring teams build features people actually want.

Can design thinking help with regulatory compliance in fintech?

Yes. While regulations set the rules, design thinking helps teams meet them in ways that feel natural for the user. By involving compliance experts early and mapping the user journey alongside legal requirements, teams can create processes that pass audits without confusing or alienating customers. For example, identity verification can be broken into smaller, clearer steps instead of one long form.

How do you measure the ROI of design thinking in fintech?

Measuring return on investment starts with defining what success looks like. For fintech products, this might mean higher completion rates in onboarding, fewer customer support requests, or faster time to market. Other signs of value include improved retention, better satisfaction scores, and reduced waste from features no one uses. Tracking these before and after applying design thinking gives a concrete view of its impact.

What are the benefits of design thinking in financial services?

Design thinking helps financial services teams create products that align with real customer needs instead of assumptions drawn purely from intuitive thinking. It can shorten time to market, improve user adoption, and reduce development waste. Design thinking can also uncover customer needs that lead to entirely new business models and reveal additional profit pools. Finally, it supports better compliance integration and stronger trust between companies and their users.

Thanks for reading!

DeepInspire / boutique software development company